Performance Attribution & Fee Management

Liquidity provision is not about chasing APR.

It is about managing inventory risk and extracting fees efficiently.

Objective

In Operational Risk, returns are estimated with weekly harvest fees. As LP are highly dynamic, we can only assume an estimated return, while realized return is computed when position is closed.

To summarize:

- Expected return -> decision support

- Realized return -> performance measurement

Fee Management Process

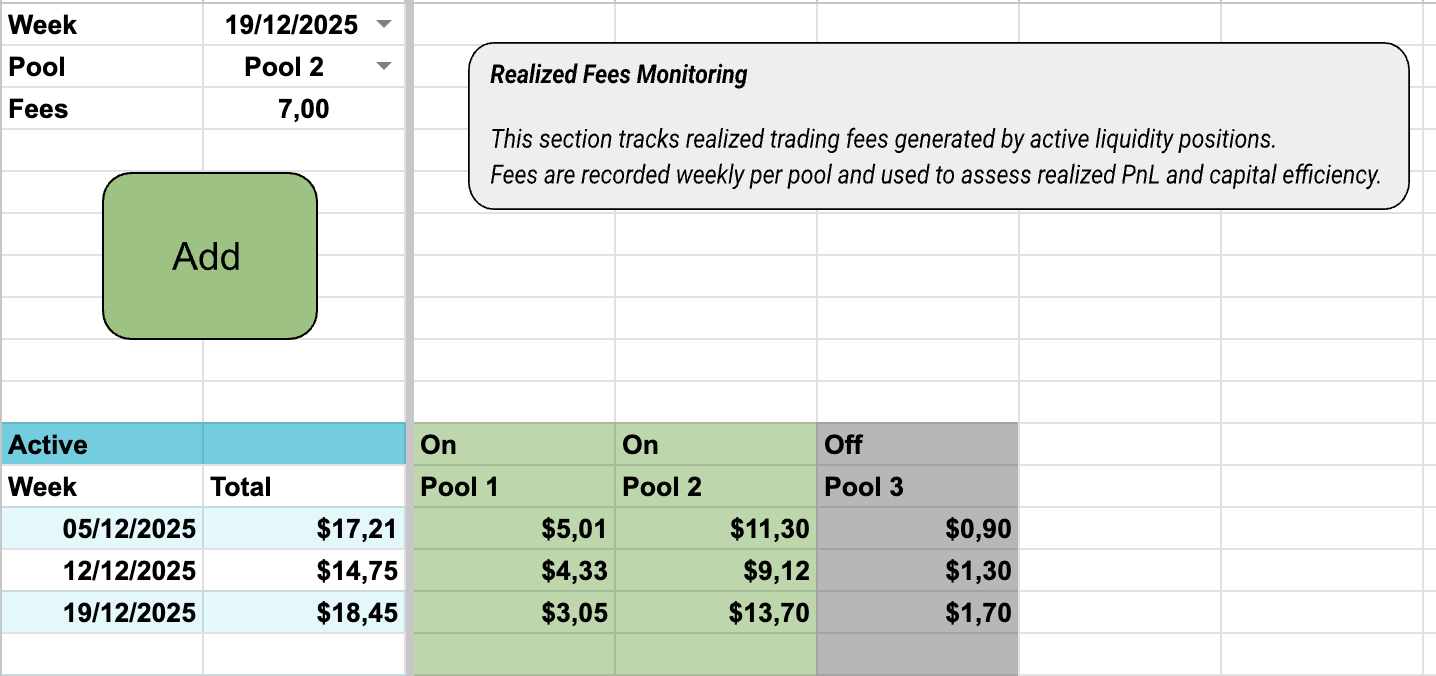

Harvested Fees tracking interface

This layer aims to track all harvested fees. It records fees from active/inactive pools by weeks -> realized fees.

All the fees-related data in the Dashboard comes from this layer.

Workflow

- Cadence: Weekly harvest (optimizing transaction costs + earnings start to be valuable)

- Simplicity : Fast input (Week, Pool, Amount). Then, It is automatically added in the table.

- Control : Only active pools and existing weeks are selectable.

Performance Measurement Framework

Net performance analysis for closed positions

To compute the overall realized return, positions must be closed.

This module shows us if the position was sufficiently compensated for the associated risk. Here is how it works:

- Captured fees (through the Fees layer).

- Inventory drift (difference between open / close).

Meanwhile Duration is used to measure the daily performance of the position.

-> Daily return allows performance comparison across positions with different lifetimes.

This module answer the crucial question: Is the compensation enough for the associated risk taken?

Why this matters

- Fees vs Management: Fees do not compensate poor range management

- Asset Selection: Picking wisely underlying crypto is essential (beware of too much vol)

- Time Sensitivity: Time matters more than expected APR

Performance without risk context is noise. This toolkit links both.